Net Worth Tracker: Why It’s the First Step to Financial Freedom

Net Worth Tracker: Why It’s the First Step to Financial Freedom

Net Worth Tracker: Why It’s the First Step to Financial Freedom

Know Your Number. Build Your Future.

1. The Foundation of Financial Awareness

Before you can master your money, you need to understand where you stand. That’s what net worth tracking is all about, taking stock of everything you own and owe, in one clear number. It’s not just a finance buzzword. It’s the starting point for nearly every serious financial plan, whether you’re paying off debt, investing for the future, or saving for retirement.

Many people go through life focusing only on income or expenses. But income can fluctuate, and budgeting, while essential, only shows what’s coming in and going out. Net worth, by contrast, offers the full picture. It answers a bigger question: are you getting ahead financially, or falling behind?

Tracking your net worth creates visibility. Whether you want to track your net worth online, get a real-time snapshot, or start using a personal finance dashboard free, it begins with understanding what you own and owe.

In this guide, we’ll explore what net worth really means, why it matters, how it differs from budgeting, and how tracking it over time can transform your financial trajectory.

2. What Is Net Worth and Why It Matters

Many people start with a basic net worth calculator, but a more effective approach is using a full net worth tracker app that updates as your finances evolve.

Assets include anything you own that has value, savings, investments, property, pensions, even valuable personal items. Liabilities are what you owe, mortgages, loans, credit card debt, and so on.

For example, if you have $40,000 in savings, a $10,000 car, and a home worth $300,000, those are your assets. If you owe $250,000 on your mortgage and $5,000 in credit cards, your liabilities are $255,000. That gives you a net worth of $95,000.

This number is a snapshot of your financial position at a given point in time. Unlike your income, which tells you how much you earn, net worth tells you how much you actually have.

Knowing your net worth can shift your mindset. You stop thinking only in terms of income or spending, and start thinking about growing long-term value. It’s the number that matters when you're building wealth.

3. Net Worth vs Budgeting: What’s the Difference?

Budgeting and net worth tracking are both essential financial tools, but they serve very different purposes.

Budgeting is about managing your income and expenses. It helps you control day-to-day spending, plan for upcoming bills, and stay within your financial limits each month. It’s like checking your speed and fuel while driving.

Net worth tracking, on the other hand, focuses on the bigger picture. It tracks your total financial position over time, showing whether your assets are growing faster than your debts. It’s like checking the health, value, and long-term performance of the whole vehicle.

You can stick to a budget and still end up with little progress toward your goals if you’re not also growing your net worth. Likewise, tracking your net worth without a spending plan may reveal problems too late.

The most effective strategy is to do both. Budgeting keeps your financial engine running smoothly. Net worth tracking tells you whether it’s taking you where you want to go. While budgeting is about control, net worth tracking supports longer-term financial planning tools for individuals, helping you assess growth, reduce liabilities, and plan smarter.

4. The Psychology of Tracking Net Worth

Tracking your net worth isn’t just about numbers, it’s about mindset. When you regularly monitor your financial position, you naturally become more intentional with your money. Spending becomes more conscious, saving feels more purposeful, and financial decisions start aligning with your long-term goals.

This simple act of tracking creates accountability. It’s common for people to reduce debt or increase savings more consistently once they start watching their net worth monthly or quarterly. You’re no longer guessing, you’re measuring.

It also builds motivation. Seeing progress, even small gains, can be incredibly rewarding. Whether your net worth increases by $200 or $2,000, that upward movement reinforces good habits and encourages you to stay on track.

In short, tracking net worth turns abstract financial goals into visible, achievable progress. And that psychological shift can be the difference between drifting financially and taking control.

5. Growth Over Time: Why Tracking Regularly Pays Off

One of the most powerful things about tracking your net worth is the ability to see progress over time. When you log your numbers monthly or quarterly, patterns start to emerge, and those patterns tell a story.

You’ll begin to see how paying off a loan, investing consistently, or cutting unnecessary expenses gradually shifts your net worth upward. These small wins compound. What looks like a modest gain each month can add up to significant progress over a year or two.

Regular tracking also keeps you responsive. If your net worth stalls or dips unexpectedly, you can investigate the cause, maybe an investment loss, rising debt, or an overlooked expense, and take action early.

Over time, this habit builds momentum. You’re no longer just hoping things improve. You’re actively shaping your financial trajectory, and watching the results unfold in real time.

6. Common Pitfalls and How to Avoid Them

While tracking your net worth is simple in principle, there are a few common mistakes that can distort your numbers or lead to false confidence. Avoiding these will keep your tracking accurate and useful.

- Overestimating asset values: Many people use optimistic figures for property, vehicles, or personal items. Use conservative, realistic valuations, not wishful thinking, especially for assets that depreciate.

- Forgetting hidden assets or liabilities: It’s easy to overlook pensions, employer stock options, or smaller debts like “buy now, pay later” accounts. Review all accounts and obligations regularly to avoid blind spots.

- Ignoring currency risk: If you hold assets in different currencies (e.g. USD stocks with a GBP base), shifts in exchange rates can impact your net worth. Consider using a consistent base currency to make tracking meaningful.

- Tracking inconsistently: Sporadic updates won’t give you a clear view. Set a reminder to update your net worth weekly, monthly or quarterly, and stick to the same format and sources for consistency.

By steering clear of these pitfalls, you’ll get a clearer, more reliable picture of your financial health, and a better foundation for decision-making.

7. Case Study: A Net Worth Journey

To bring it all to life, let’s look at a simplified case study.

Case Study

Meet Jane, a 35-year-old freelancer living in the US. When she first started tracking her net worth, she had a modest income, some student loan debt, and a few scattered savings accounts.

Her starting net worth was $2,400, made up of:

- $6,000 in savings

- $3,600 in credit card debt

Over time, Jane took several small but strategic steps:

- Paid off her credit card debt over 12 months

- Built an emergency fund of $10,000

- Contributed $6,000 per year to a retirement account (total: $18,000)

- Invested $5,000 in a low-cost index fund

- Tracked her second-hand car as a depreciating asset, currently valued at $3,500

- Built $4,000 in retained profits from a part-time side business

- Continued saving an extra $2,800 across miscellaneous accounts

Three years later, her total assets had grown to $49,300, with no debt. Here’s the breakdown:

- Emergency Fund: $10,000

- Retirement Account: $18,000

- Index Fund Investment: $5,000

- Side Business Balance: $4,000

- Savings: $2,800

- Vehicle (current value): $3,500

- Other personal assets: $6,000

Total Net Worth: $48,700

By starting with a simple free net worth tracker, Jane was able to build structure into her finances and track progress across assets, debts, and investments. Jane’s journey shows how consistent tracking, even with a modest income, leads to real progress. Her visibility into finances helped her make smarter choices and stay focused, proof that financial freedom doesn’t start with wealth, it starts with awareness.

8. Final Thoughts: Financial Freedom Starts with Visibility

Most people think financial freedom begins with earning more. In reality, it begins with understanding what you already have, and what you owe. That’s why tracking your net worth is such a powerful habit. It gives you clarity. It builds momentum. And it transforms vague goals into measurable progress.

Whether you're starting with a positive number, a negative one, or something close to zero, what matters most is consistency. Month by month, you’ll start seeing the effects of your financial decisions, and that feedback loop is what creates real change.

Net worth tracking isn’t about perfection. It’s about direction. And the sooner you start, the faster you gain control.

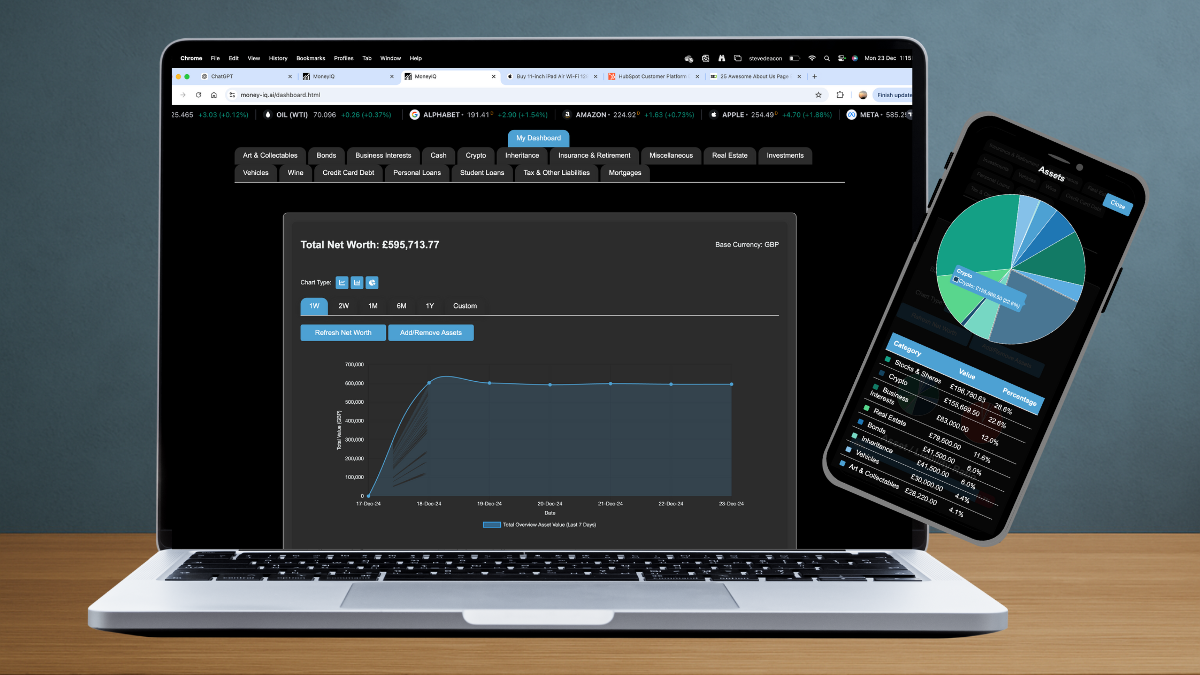

9. How MoneyIQ Can Help

If you're ready to track your net worth online but want a faster, smarter way to do it, MoneyIQ can help. Our platform makes it easy to record your assets and liabilities, monitor changes over time, and use AI tools for retail investors to stay on top of your goals.

The core net worth tracker is completely free, no credit card required with our Basic Tier. You’ll also get access to AI investing tools designed for beginners, making it easier to analyze companies for investing or compare stocks using key ratios.

Want to go further? Use MoneyIQ’s AI to generate stock reports with AI, run automated company analysis for beginners, and dive deep into financial ratio analysis and interpretation,all in one streamlined dashboard.

Financial freedom starts with knowing your number. Let MoneyIQ help you take the first step.