Tax Loss Harvesting for UK Investors

Tax Loss Harvesting for UK Investors

Tax Loss Harvesting for UK Investors

Introduction: Tax Loss Harvesting for UK Investors

In today’s ever-changing market, finding smart ways to reduce your tax bill is more important than ever. Tax loss harvesting—selling assets that haven’t performed well to offset gains elsewhere—can be a real game-changer for UK taxpayers, especially as we look ahead to the new tax year starting on 6th April 2025.

By carefully managing your portfolio and timing your sales, you can potentially lower your overall tax liability and boost your long-term returns. This guide walks you through the essentials of tax loss harvesting, explains its benefits, and shows you how to put these strategies into practice under the latest UK tax rules.

We’ll cover everything from the basic concepts and process overview to practical implementation tips and the legal and regulatory nuances that impact how losses are claimed. And if you're following along from overseas, we’re also preparing a similar piece tailored specifically for US taxpayers—so stay tuned!

With the new tax year just around the corner, effective tax loss harvesting strategies can help investors reduce capital gains tax liabilities and optimize portfolio performance.

Overview of Tax Loss Harvesting: Key Concepts and How It Works

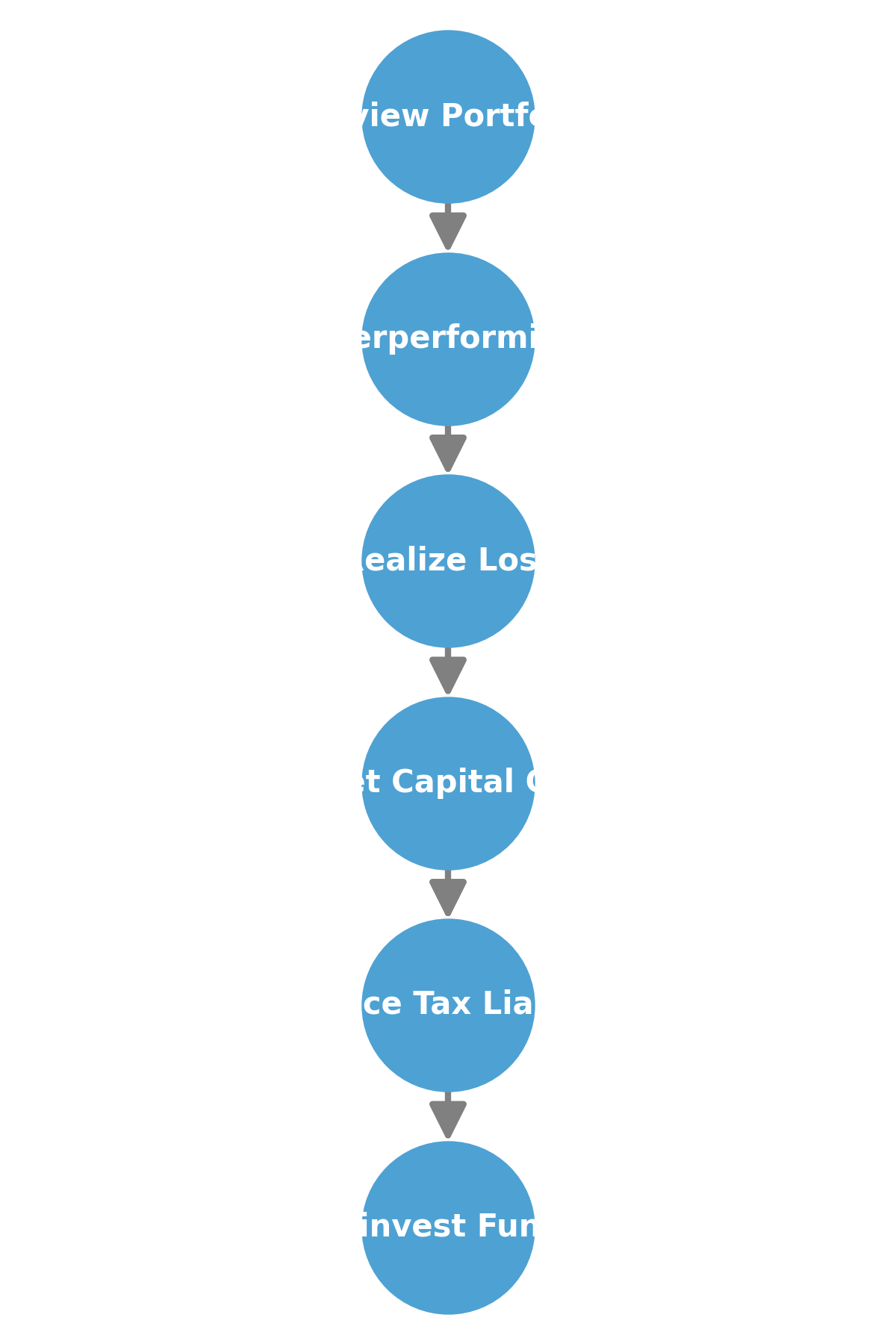

The tax loss harvesting process begins with a careful review of your portfolio to identify assets that have declined in value. Selling these underperforming investments realises a loss, which can then be applied against gains from other transactions within the tax year—thus lowering your net taxable income.

Typically, after selling the selected assets, many investors opt to reinvest the proceeds into similar or alternative investments. This reinvestment not only maintains your desired asset allocation but also positions your portfolio for potential future growth. Note that there are specific rules regarding which assets and funds can be reinvested—and when—after a loss disposal. We will cover these rules in detail later in the article.

The diagram on the right visually outlines the 6 stage process flow, from portfolio review and sale to loss realisation, offset and reinvestment.

In the next section, we will transition to an examination of the latest UK tax law updates and regulations, which further shape how these strategies can be effectively implemented.

Implementing Tax Loss Harvesting: Strategies Tailored for UK Retail Investors

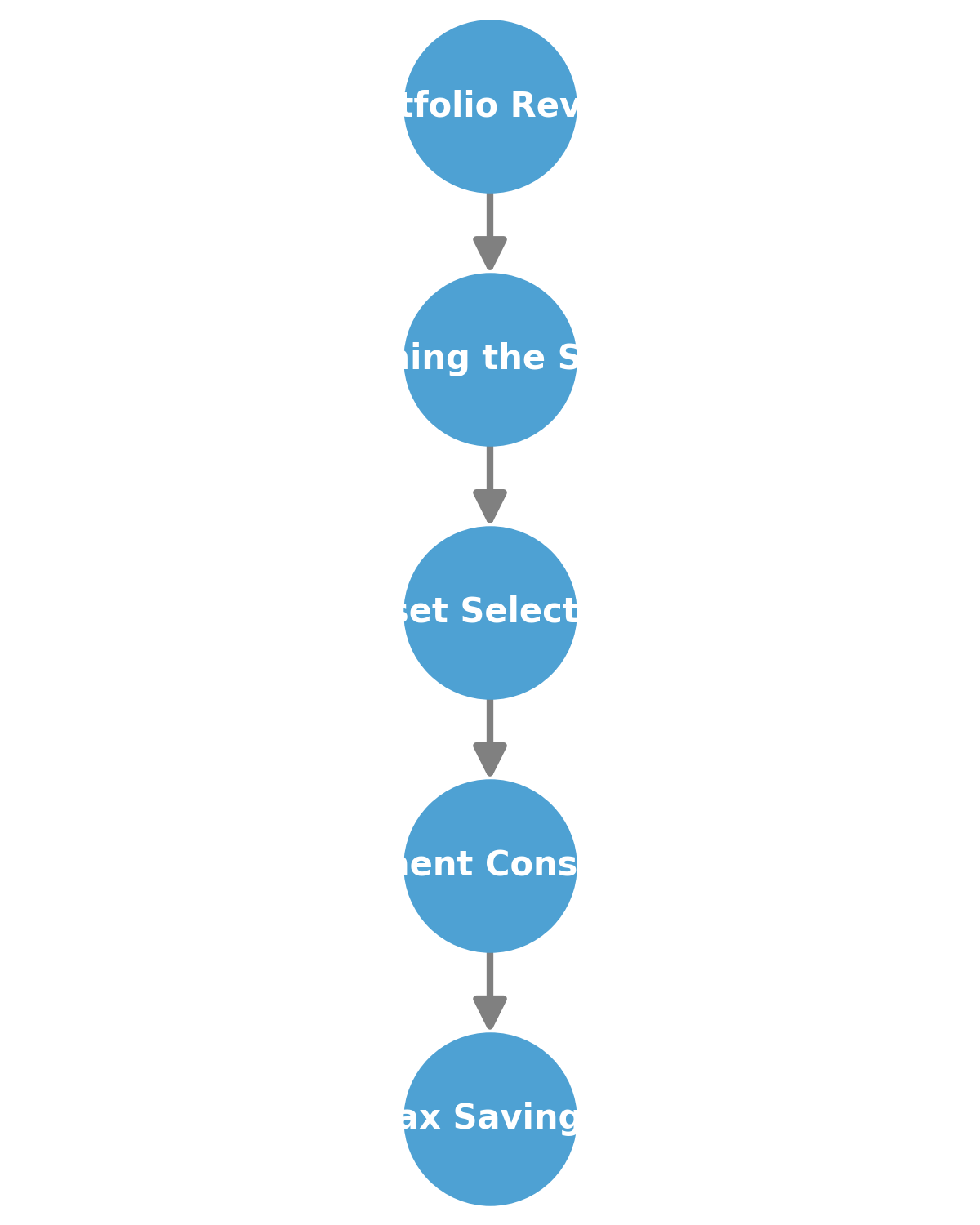

Executing tax loss harvesting effectively starts with a systematic review of your portfolio. Begin by identifying underperforming assets that have declined in value and assess if selling these assets aligns with your overall investment strategy.

Step 1: Portfolio Review – Conduct a detailed analysis of your holdings to identify assets with sustained losses, considering market trends and your long-term goals.

Step 2: Timing the Sale – Timing is critical. Avoid selling solely based on short-term market volatility. Instead, use market data and technical indicators to choose the optimal moment to realise losses.

Step 3: Asset Selection – Not every loss should be harvested. Focus on assets that no longer fit your strategy or are unlikely to recover in the short term, thus preserving quality investments while improving your tax position.

Step 4: Reinvestment Considerations – After realising losses, consider reinvesting proceeds into similar or diversified assets. This helps maintain your desired asset allocation and positions your portfolio for future growth. Remember, certain wash sale rules may apply that could affect the validity of your loss – we will discuss these rules in detail in the next section.

Retail investors are encouraged to adapt these strategies to their unique portfolios and market conditions, using this guide as a foundation for reducing taxable gains.

Legal Considerations: Wash Sale Rules, Anti-Avoidance Measures, and Asset-Specific Nuances

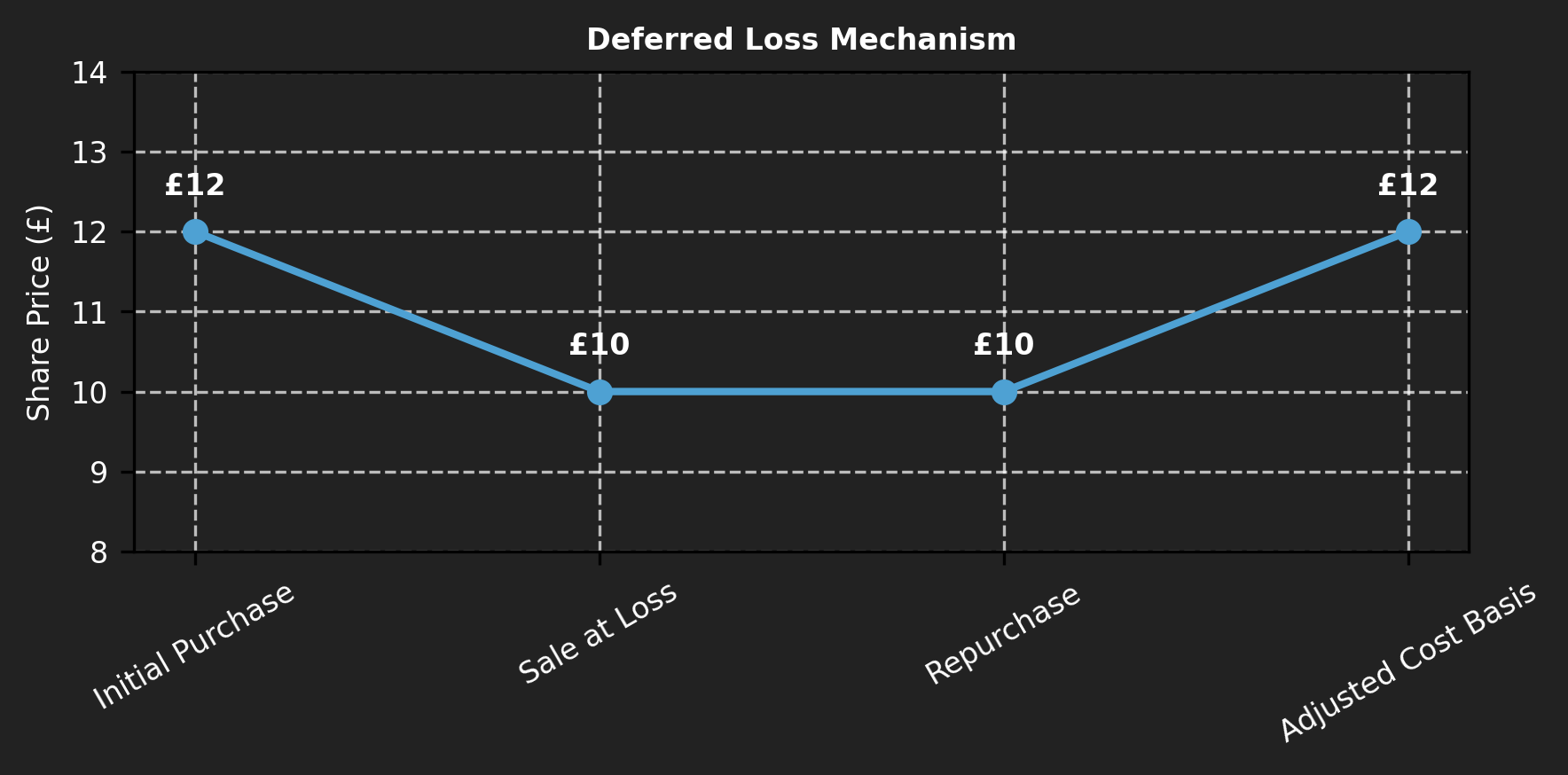

In the UK, while there isn’t a statutory “wash sale” rule like in the US, HMRC enforces strict anti-avoidance measures—most notably the “replacement of assets” rule. If you sell shares or cryptoassets at a loss and then repurchase substantially identical assets within 30 days, HMRC will adjust the cost basis of the repurchased assets, effectively deferring the loss.

Additionally, HMRC requires that all transactions are accurately reported on your Self Assessment tax return. Investors must retain detailed records from their brokers or exchange platforms to substantiate any losses claimed. These measures ensure that only genuine losses are used to offset taxable gains.

It is important to note that while equities benefit from standardized pricing and detailed transaction records, cryptoassets can exhibit higher volatility and variable pricing across different exchanges. As a result, the same anti-avoidance measures apply to both, but record-keeping and valuation require extra care with crypto.

Example: Anti-Avoidance in Action

Example: Suppose an investor holds 100 shares of Company X, purchased at £12 per share. When the market price falls to £10 per share, the investor sells all 100 shares, thereby realising a total loss of £200 (100 x (£12 - £10)). If the investor then repurchases 100 shares of Company X within 30 days at £10 per share, HMRC will apply its anti-avoidance rule. Instead of allowing the £200 loss to offset gains in that tax year, HMRC adjusts the cost basis of the repurchased shares. In this case, the new cost basis is calculated as the repurchase price plus the deferred loss per share, resulting in a revised cost basis of £10 + (£200/100) = £12 per share. The loss is effectively deferred until the investor sells these repurchased shares at a future date.

Furthermore, regulatory factors—such as specific reporting requirements and restrictions on reinvestment—are critical. Investors should also monitor ongoing debates, such as whether Capital Gains Tax should “die with you,” as future legislative changes may impact these rules.

Please note: The legal framework described here reflects current HMRC guidance. Laws and regulations can change, so it is essential to stay updated with the latest official publications and seek professional advice.

In the next section, we will present case studies focusing separately on equities and cryptoassets to illustrate how these legal considerations affect tax loss harvesting in real-world scenarios.

Case Studies: Tax Loss Harvesting in Shares and Crypto

Although shares and cryptoassets are both treated as capital assets for tax purposes in the UK, subtle differences—such as the application of the “bed and breakfast” rule and share pooling—can influence tax loss harvesting outcomes. Below are two case studies, each with three scenarios detailing the investor’s actions and the tax treatment.

Case Study 1: Shares (Unilever PLC)

Scenario Setup: A UK investor purchased 100 shares of Unilever PLC at £50 per share, investing a total of £5,000. Due to market volatility, Unilever’s share price later falls to £45. The investor sells 50 shares at this lower price, realising a loss of £250 (50 x (£50 - £45)). The following scenarios show different actions the investor could take and the resulting tax treatment.

Scenario 1: Sell and Do Nothing

Example: The investor sells 50 shares at £45 per share, realising a £250 loss. With no repurchase, the full £250 loss is immediately available to offset other taxable gains. For example, if the investor has £500 in gains from other investments, the net taxable gain would be £250, saving approximately £50 at a 20% tax rate.

Scenario 2: Sell & Repurchase Same Asset

Example: The investor sells 50 shares at £45 per share, realising a £250 loss, then repurchases the same 50 shares within 30 days at £45. HMRC’s anti-avoidance rule defers the loss by adding £250/50 = £5 per share to the repurchase price, so the new cost basis becomes £45 + £5 = £50 per share. The loss benefit is deferred until these shares are eventually sold.

Scenario 3: Sell & Reinvest in an Alternative Asset

Example: The investor sells 50 shares at £45 per share, realising a £250 loss, and reinvests the proceeds in another UK blue-chip, such as GlaxoSmithKline PLC. Since the new asset isn’t considered substantially identical to Unilever, HMRC permits the full £250 loss to be claimed immediately. If the investor has £500 in gains from other investments, the taxable gains reduce to £250, yielding an approximate tax saving of £50 at a 20% rate.

Case Study 2: Cryptoassets (Bitcoin)

Scenario Setup: A UK investor purchases 5 BTC at $100,000 each. With a purchase exchange rate of 1.23, the cost per BTC is approximately £81,300, for a total investment of around £406,500. Later, Bitcoin’s price falls to $95,000. With a sale exchange rate of 1.25, the sale price per BTC becomes £76,000. The investor sells all 5 BTC, realising total proceeds of £380,000 and a loss of approximately £26,500.

Scenario 1: Sell and Hold

Example: The investor sells 5 BTC at £76,000 each, realising a total loss of £26,500. With no repurchase, the full loss is immediately available to offset other gains. For example, if the investor has £50,000 in gains from other assets, the net taxable gain becomes £23,500, resulting in a tax saving of approximately £5,300 at a 20% rate.

Scenario 2: Sell & Repurchase Identical Crypto

Example: The investor sells 5 BTC at £76,000 each, realising a loss of £26,500, and repurchases 5 BTC within 30 days at £76,000. HMRC’s anti-avoidance rule defers the loss by adding a deferred loss of £26,500/5 = £5,300 per BTC to the repurchase price. The adjusted cost basis becomes £76,000 + £5,300 = £81,300 per BTC, deferring the tax benefit until these BTC are sold.

Scenario 3: Sell & Reinvest in a Different Crypto

Example: The investor sells 5 BTC at £76,000 each, realising a loss of £26,500, and reinvests the proceeds in Ethereum. Since Ethereum is not considered substantially identical to Bitcoin, HMRC permits the full £26,500 loss to be claimed immediately. If the investor has £50,000 in gains from other assets, the taxable gain is reduced to £23,500, resulting in a tax saving of approximately £5,300 at a 20% rate.

These case studies illustrate that while the loss deferral mechanism is broadly similar for shares and cryptoassets, practical differences—such as record-keeping challenges and specific share identification rules—can lead to different tax outcomes. In the next section, we will discuss tools and resources to help you implement these strategies effectively.

Tools & Resources

Implementing a successful tax loss harvesting strategy requires the right tools and resources. Below are some recommended links and services to help you navigate UK tax rules and optimize your investment strategy:

- HMRC Capital Gains Guidance: Check the official HMRC website for the latest information on tax rates, allowances, and reporting requirements.

- Investment Tracking & Tax Tools: Stay tuned for upcoming MoneyIQ calculators for Capital Gains Tax and Tax Loss Harvesting, which will help you estimate your liabilities and potential savings.

- Track Your Investments: MoneyIQ offers a comprehensive platform to track your investments and analyzing performance. Get started by opening an account today.

- Professional Advice: Consider consulting a qualified tax advisor who specializes in investment taxation to ensure your strategy complies with current HMRC legislation.

These resources can help you stay informed and make well-informed decisions when implementing your tax loss harvesting strategy.

Conclusion & Actionable Insights

Tax loss harvesting is a powerful strategy for UK investors, enabling you to reduce your tax liability and optimize your portfolio. By understanding the key concepts, keeping up-to-date with evolving UK tax laws, and applying practical strategies, you can effectively manage your gains and losses.

Here are some actionable steps to help you get started:

- Review your portfolio to identify underperforming assets.

- Determine if selling these assets aligns with your long-term investment goals.

- Familiarize yourself with HMRC’s rules on loss harvesting, including repurchase timing and reporting requirements.

- Use available tools and resources, like MoneyIQ to calculate potential tax savings.

- Consult a tax professional to ensure your strategy remains compliant with the latest legislation.

Remember, tax laws can change, so it's essential to stay updated with the latest HMRC guidance and adjust your strategy accordingly.

Take control of your financial future with MoneyIQ. Track your net worth in real-time, gain AI-powered insights, and make smarter financial decisions. Get started today and take the first step toward financial freedom.

Disclaimer

This article is for informational purposes only and should not be considered financial advice. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions.

MoneyIQ Team