Understanding Bonds in Today’s Market

Understanding Bonds in Today’s Market

Understanding Bonds in Today’s Market

Investing in bonds can be a great way to build a stable, predictable income while diversifying your portfolio. Whether you’re new to investing or looking to refine your strategy, understanding bonds will help you make informed financial decisions. So, let’s break it down and explore why bonds are an essential investment.

Understanding bonds: a stable investment option in today’s volatile markets.

What Are Bonds?

Think of a bond as a loan, but instead of lending money to a friend, you’re lending it to a government or a company. In return, they promise to pay you interest regularly and then give you back the full loan amount when the bond matures.

For example, if you purchase a bond for $1,000 with a 5% coupon rate, you’ll receive $50 every year until the bond reaches maturity. At that point, you’ll get back your original $1,000.

Bonds are often seen as less risky than stocks because they provide predictable returns. However, they do come with risks, such as changes in interest rates and credit defaults, which we’ll discuss later.

How Do Bond Payments Work?

When you invest in a bond, you earn interest based on the coupon rate. This interest is a fixed percentage of the bond’s face value.

For example, if you buy a U.S. Treasury bond (CUSIP: 912828V80) for $1,000 with a 3% coupon rate and a 10-year maturity, you’ll receive $30 annually ($1,000 × 3%) until the bond matures. Once it does, you’ll also get back your original $1,000.

Corporate bonds work similarly but often offer higher returns. A bond from Apple Inc. (AAPL 3.25% 2027, CUSIP: 037833CG3) might provide a slightly higher yield than government bonds because corporations pose a greater risk than governments.

Comparing Bond Coupon Payments

| Bond Type | Face Value | Coupon Rate | Annual Interest | Years to Maturity | Total Interest Earned |

|---|---|---|---|---|---|

| U.S. Treasury Bond | $1,000 | 3% | $30 | 10 | $300 |

| Apple Corporate Bond | $1,000 | 3.25% | $32.50 | 5 | $162.50 |

| Tesla Corporate Bond | $1,000 | 5.30% | $53 | 7 | $371 |

U.S. Treasury bond data and Apple bond data sourced from official issuer websites. Tesla bond rate is hypothetical, used for illustrative purposes.

How Are Bonds Priced?

Bonds aren’t always sold for their face value. Their price changes depending on market interest rates and investor confidence.

If market interest rates rise, your bond’s value may drop because newer bonds offer higher rates. On the flip side, if rates fall, your bond becomes more attractive, increasing its value.

Let’s say you own a bond that pays 5% interest, but new bonds are being issued at 6%. Investors will prefer those new bonds, which makes your bond worth less. However, if new bonds offer only 4%, your 5% bond is now more valuable.

Bond Prices and Market Interest Rates

| Market Interest Rate | Bond Coupon Rate | Bond Price | Investor Demand |

|---|---|---|---|

| 4% | 5% | Above $1,000 (Premium) | High |

| 5% | 5% | $1,000 (Par Value) | Neutral |

| 6% | 5% | Below $1,000 (Discount) | Low |

The bond pricing and interest rates in this table are for illustrative purposes only and do not represent real-time market data.

Yield to Maturity: What Are You Really Earning?

Your return on a bond isn’t just about the coupon rate. If you buy a bond at a discount or premium, your actual return—called yield to maturity (YTM)—will be different.

Say you buy a $1,000 bond at $950. You still receive interest based on the original $1,000 value, meaning your actual return is higher than the coupon rate. If you buy it at $1,050, your return is lower because you’ll only receive $1,000 when the bond matures.

Most investors use financial tools to calculate YTM, but the main idea is that your real return depends on both the coupon payments and the price you paid for the bond.

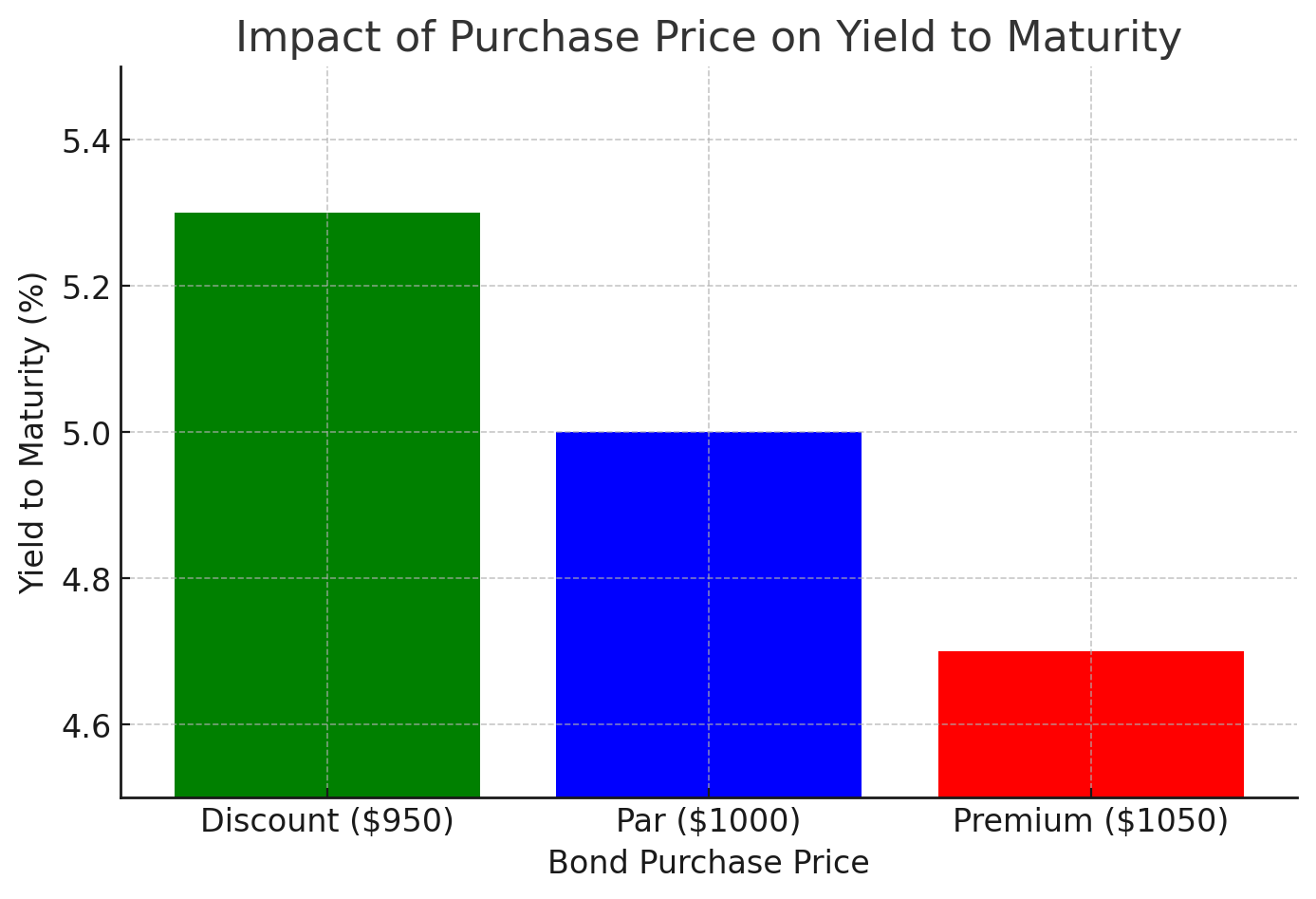

How Purchase Price Affects Yield to Maturity

Yield to Maturity (YTM) changes depending on whether you buy a bond at a discount, face value, or premium. Here’s how different purchase prices impact YTM:

As shown in the chart:

- Buying at a discount ($950) results in a higher YTM (5.3%), as you're earning more compared to the initial investment.

- Buying at par ($1,000) gives a YTM equal to the coupon rate (5%).

- Buying at a premium ($1,050) lowers your YTM (4.7%) since you’re paying extra upfront.

The YTM rates shown are for illustrative purposes only and do not represent real-time bond market data.

Government Bonds vs. Corporate Bonds

Government bonds are considered some of the safest investments. If security is your priority, you might consider U.S. Treasury Bonds (CUSIP: 912810SV1). They are backed by the U.S. government, making them low-risk.

Other options include UK Gilts (GB00BMBL1M60), issued by the British government, and German Bunds (DE0001102507), which offer stability but lower yields.

Corporate bonds typically provide higher returns to compensate for added risk. For example, a bond from Tesla Inc. (TSLA 5.30% 2028, CUSIP: 88160RAN5) offers a higher yield, reflecting Tesla’s rapid expansion and associated risks. Similarly, a bond from HSBC Holdings (HSBC 6.375% 2033, ISIN: US404280BT82) provides a competitive yield with more stability.

The High-Risk World of Junk Bonds

Junk bonds, also called high-yield bonds, offer bigger interest payments but come with significant risk. These bonds are issued by companies with lower credit ratings, meaning they have a higher chance of default.

Take WeWork (WEWKQ 7.875% 2025, CUSIP: 96209AAB4) as an example. They issued junk bonds to raise capital despite their financial struggles. The potential returns were attractive, but investors faced a serious risk of default.

Risks to Consider

Although bonds are generally safer than stocks, they aren’t risk-free.

One major risk is interest rate changes. If rates rise, your bond’s value drops. This isn’t a problem if you hold the bond until maturity, but if you plan to sell early, you could lose money.

There’s also credit risk—the possibility that the issuer won’t make payments. Government bonds are typically low-risk, but corporate bonds vary based on the company's financial health.

Inflation is another factor. If inflation increases, your fixed bond payments lose purchasing power. A 5% return sounds good until inflation is also 5%, effectively wiping out your gains.

Should You Invest in Bonds?

Bonds are an excellent way to balance your investment portfolio, providing stability in uncertain times. Government bonds are great for conservative investors, while corporate bonds offer higher returns for those willing to take on more risk.

Before investing, consider market interest rates, inflation, and your overall portfolio strategy. A mix of government and corporate bonds can help you manage risk while maintaining steady returns.

Final Thoughts

Understanding bonds is key to making smart investment choices. Whether you’re looking for security or higher yields, knowing the different types of bonds and their risks will help you build a strong financial future.

Want to take control of your financial future? MoneyIQ helps you optimize your net worth and gain valuable insights into smart money management. Click the "Get Started" button at the top of this page to begin your journey today!

Disclaimer

This article is for informational purposes only and should not be considered financial advice. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions.

MoneyIQ Team